|

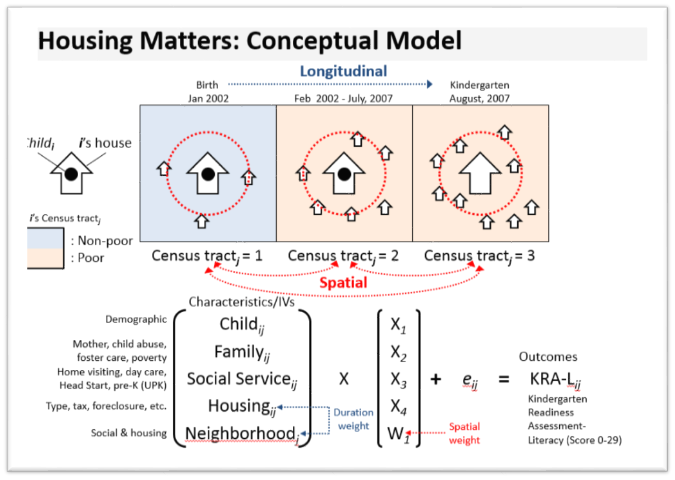

The Poverty Center is tapping into Big Data, learning more about the

housing crisis and its impact on American children. |

Well over 80 million people

tuned in for the face off, setting a new record in the sixty-year history of

televised presidential debates. Among

them, 62% are still “with her,” standing by her man, to make America “Stronger

Together.” Contrary to populist

perception, scientific polling suggests that only 22% are still in that “basket

of deplorables” with him to “Make America Great Again.” According to National

Public Radio, actual scientific polls have shown that Clinton was the clear

winner in Monday night’s televised debate.

The presidential hopefuls’

quest to occupy public housing at 1600

Pennsylvania Avenue rent-free has some beleaguered homeowners wondering if

the two-party system has run its course. This

is just one reason why voters need to see all candidates’ income tax returns.

The current residents at The

White House, an upwardly mobile African American family, will be headed back to

the block with a handful of explanations as to why simple stuff like the

mortgage crisis has yet to be resolved for everyday Americans.

One could claim that as the

first African American president, Barack Obama did all he could to restore

America’s economy. He counseled his

predecessor on the Wall Street Bail Out, super-glued Freddie Mac’s and Fannie

Mae’s brokenness, and got the auto industry back up and running--ALL without

urgently needed appropriations bills from Congress.

But, a decision not to

investigate, prosecute and imprison former Vice President Dick Cheyney, select

cabinet members and advisors from a previous administration may prove to be the

one executive action defining two otherwise productive terms. Both the Bush and the Obama Administrations

knew about Cleveland,

Ohio’s housing problem.

The

American Mentor Wire Service, a program of Youth Achievers USA Institute, started

observing economic trends and behaviors as far back as 1998. That was the year young Americans called for

a 10-year Million

Youth Movement. They met in Atlanta,

GA and set goals around their individual and collective visions for the

future. Among the less than a million

committed souls were beneficiaries of an American Civil Rights era. They were banking on an inheritance that somehow

resulted instead in a compromise on a long-overdue

promissory note.

By 2008, the hope of

disadvantaged Americans owning their first homes had faded in the cloud of a

seven-year mortgage crisis. Two

government-sponsored enterprises (GSE), Fannie

Mae and Freddie Mac,

suffered large losses and were seized by the federal government the summer of

2008 as two-party presidential campaigning shifted into business as usual. President Bush attempted to ease concerns with

an observation that “the

economy is fine.”

Earlier, in order to meet

federally mandated goals to increase homeownership, Fannie Mae and Freddie Mac

had issued debt to fund purchases of subprime mortgage-backed securities, which

later fell in value. In addition, the

two government enterprises suffered losses on failing prime mortgages, which

they had earlier bought, insured, and then bundled into prime mortgage-backed

securities that were sold to investors.

Historically, potential

homebuyers found it difficult to obtain mortgages if they had below average

credit histories, provided small down payments or sought high-payment loans. So, as some wealthy Americans benefitted from

the G.W. Bush era tax cuts, few of them ever bothered to follow through on

their obligations through the New Market

Tax Credits Act.

Not everybody is an economist,

and most economists you meet are more concerned with their next paycheck than

your bottom line. But, in a nutshell, the

September 6, 2008 conservatorship to balance Freddie and Fannie’s books cost

taxpayers bigtime. Freddie and Fannie

are "independent" corporations and not federal agencies. Their combined balance sheet obligations were

just over $5 trillion, a significant amount when compared to the $9.5 trillion

of officially reported United States public debt at the time of the

Freddie-Fannie takeover.

It appears that none ($0) of

the U.S. Treasury’s infusion of capital for Freddie and Fannie helped folks

that could not qualify for Freddie and Fannie’s help in the first place. HARP seemed to be a necessary first step

toward doing the right thing, but imagine being told you don’t qualify for a

mere $100,000.00 in relief after Freddie and Fannie denied you a

government-backed loan. Then, go back

and review half the political promises made to get you a job or help you start

a business. Factor in some seemingly

unrelated issues such as implicit

biases and racial anxiety. Finally,

you’ll want to multiply your own undervaluation by 240 years of economic

compromise.

This is just one formula, to

begin quantifying a debt due to historically disadvantaged Americans. Just imagine what might have been achieved

had the U.S. Congress approved the President’s budgets over the last eight

years.

Several government agencies under

the Obama Administration took steps to increase liquidity within Fannie Mae and

Freddie Mac.

· Federal Reserve purchases of $23 billion in GSE debt

(out of a potential $100 billion) and $53 billion in GSE-held mortgage backed

securities (out of a potential $500 billion).

· Federal Reserve purchases of $24 billion in GSE debt.

· Treasury Department purchases of $14 billion in GSE

stock (out of a potential $200 billion).

· Treasury Department purchases of $71 billion in

mortgage backed securities.

· Federal Reserve extension of primary credit rate for

loans to the GSEs

Keep in mind that government-sponsored

enterprise (GSE) is a financial services corporation created by the United

States Congress. Their intended function is to enhance the flow of credit to

targeted sectors of the economy and to make those segments of the capital

market more efficient and transparent, and to reduce the risk to investors and

other suppliers of capital.

Meanwhile, way too many

Americans are still struggling with upside down mortgages, limited job

opportunities and almost no understanding of their unique small business

needs. There has always been some logic

in the belief that poor people can stop being poor as rich people are willing

to become even richer at a slower pace.

But, more than 4 million Americans don’t own homes, they own

mortgages!

According to one real estate

source, American “homeowners” owe at least 20% more than their homes are worth,

totaling $579 billion of so-called negative equity. The next President of the United States will

need to forgive

some citizens of that debt instead of compounding the issue with more empty

promises and ineffective programs. Too

many families are in serious financial crisis, while our political candidates,

members of Congress, and other elected or appointed officials mimic episodes of

“Scandal,” “Survivor,” “Empire,” or even “The Apprentice.” It’s time to stop stalling critical funding,

projects, legislation and appointments. And,

it’s past time for Congress to approve a budget.